How The EcoSaver Mortgage works

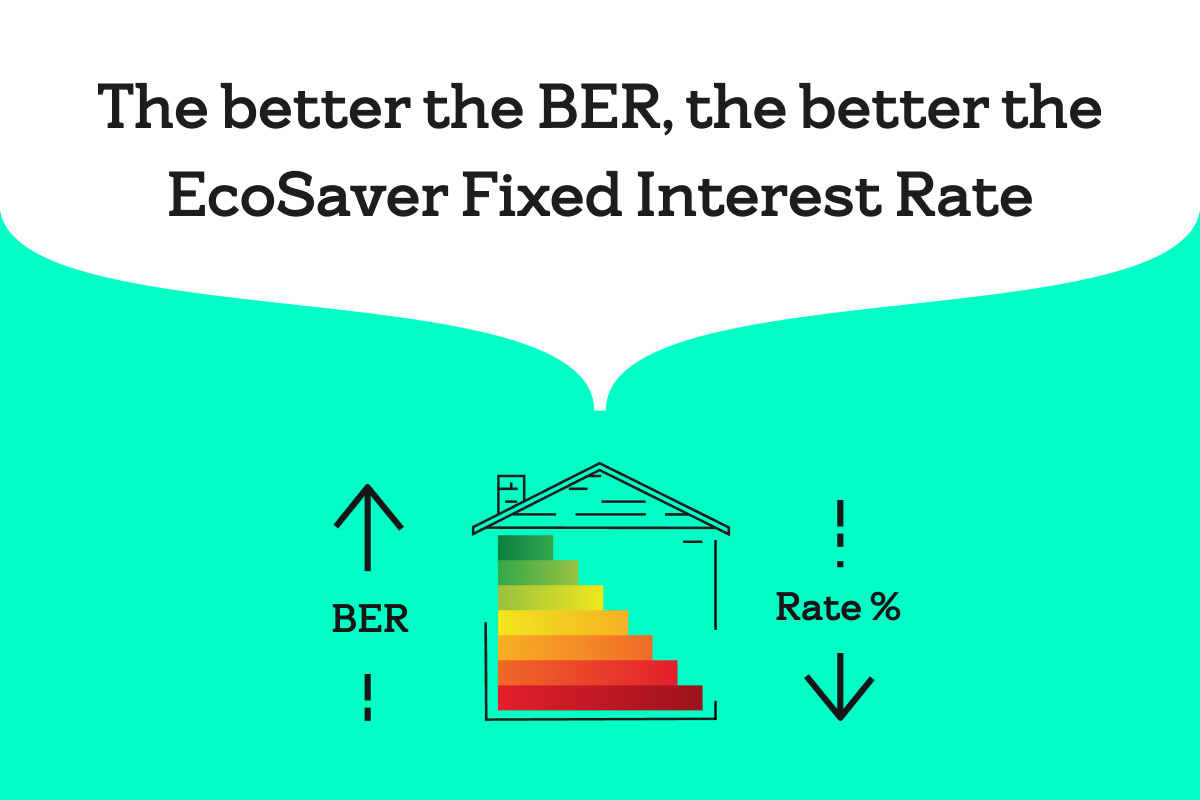

Provide your Building Energy Rate (BER) to get your EcoSaver Mortgage fixed interest rate.

Every time you complete energy upgrades and your BER goes up a letter, we’ll bring your EcoSaver Mortgage rate down* – just submit your BER certificate.

*Subject to terms and conditions

Self-Build

Home Movers

MortgageSaver

Why choose Bank of Ireland?

Cashback Plus

Get 2% of your mortgage back as cash up front, plus 1% extra in 5 years(subject to meeting the conditions of the mortgage).2

Flexi-Options

![]()

We want to help you to make the most of your mortgage. Have a look at how you can flex your mortgage to suit your lifestyle with our Flexi-Options.

Rates

Choose from our range of competitive fixed and variable interest options include fixed rates between 1 year and 10 years.

Your step by step guide to buying your first home.

Wondering how to get started with a Mortgage? All the information you need is in our First Time Buyers Guide.

Mortgage Media Hub

Explore our mortgage media hub for informative videos and podcasts covering everything you need to know about mortgages. Get expert insights and advice to guide you through your mortgage journey.

Mortgage Application Process

Step 1: Find out how much you can borrow

With our easy-to-use mortgage calculator you’ll get an indication of how much you could currently afford to borrow.

Step 2: Talk to our mortgage specialists

Make an appointment with a mortgage specialists in one of our branches or they can contact you at a time that suits you best.

Step 3: Save for your mortgage deposit

If you’re a first-time buyer, you can apply for a mortgage of up to 90% of the value of a property. Remember there are other expenses such as stamp duty, legal fees, home insurance and life cover – so you’ll need to save for those costs too.

Our MortgageSaver account1 is designed to help you save the deposit for your home.

Step 4: Start your application

When you have your deposit saved, it may be time to apply for your mortgage. You don’t have to have a property in mind at this stage.

Once you have started your application we’ll give you an outline of how much we could lend you based on the information you have provided (we call this a First Step Approval in Principle). We’ll also give you a list of the documents – salary information, bank statements, etc. – that you’ll need to provide so that your application can be fully assessed.

Step 5: Provide requested documents

Mortgage lenders generally want to see proof of your income and a record of your finances.

That means you’ll have to gather up documents like your payslips if you are employed and your most recent 2 years’ audited accounts if you are self-employed. If your accounts are not with Bank of Ireland you’ll also need to provide the last 6 months’ of your current account statements and 12 months’ savings account statements demonstrating regular saving. You can find a full list of the documents here.

When you have provided all of the documentation needed to assess your application we’ll send you an acknowledgement of this too.

Step 6: Get Approval in Principle

When your application is successful we’ll send you a formal ‘Approval in Principle’ letter. This means your loan is approved and you can go house shopping confident that your finance is in place. This approval generally lasts for 6 months.

Approval in Principle however is not a loan offer so you can’t rely on it to enter into a sale contract.

Step 7: Find a home & complete your application

When you have found a suitable property and your offer is accepted, get back in touch with us and we can finalise your mortgage application. We’ll then send you a formal Mortgage Loan Offer to buy your new property along with details of any final requirements before you can draw down your mortgage loan.

For example, you’ll need to have a valuation carried out on the property by a valuer that we approve. We also always recommend that you get a property survey carried out for your own peace of mind as this can identify potential issues that you mightn’t otherwise see.

Step 8: Complete the purchase & get your keys

Once all is in order, your solicitor will draw down your mortgage funds and arrange to transfer the property title on your behalf.

Frequently Asked Questions

Ready to move ahead?

Book an appointmentApply online

You can also request a callback or give us a call on 0818 365 345.

Our phone lines are open at the following times:

Monday – Friday: 9am – 5pm

The lender is Bank of Ireland Mortgages. Lending criteria and terms and conditions apply. A typical mortgage to buy your home of €100,000 over 20 years with 240 monthly instalments costs €613.16 per month at 4.15% variable (Annual Percentage Rate of Charge (APRC) 4.3%). APRC includes €150 valuation fee and mortgage charge of €175 paid to the Property Registration Authority. The total amount you pay is €147,482.50. We require property and life insurance. You mortgage your home to secure the loan. Maximum loan is generally 3.5 times gross annual income (4 times gross annual income for first time buyers) and 90% of the property value. A 1% interest rate rise would increase monthly repayments by €53.89 per month. The cost of your monthly repayments may increase – if you do not keep up your repayments you may lose your home. Available to over 18s only. APRC calculations are based on the cost per month on a €100,000 mortgage over 20 years.

Bank of Ireland Mortgage Bank u.c. trading as Bank of Ireland Mortgages is regulated by the Central Bank of Ireland.